|

⏱️ Estimated time to read:

A credit score is a number that shows how likely you are to repay borrowed money. [1] It usually falls between 300 and 850. Lenders use this number because it gives them a quick way to estimate risk. They want to know if you will make payments on time.

Your score comes from the information in your credit report. Scoring systems read that information and turn it into a number. Many lenders use the FICO scoring model, but other models exist. Each one uses similar ideas to judge your past borrowing behaviour.

A higher score signals lower risk. It tells businesses that you have managed credit well in the past. As a result, you may find it easier to get a loan or a credit card. You may also receive better terms, including a lower interest rate.

A lower score signals higher risk. It tells businesses that lending to you carries more uncertainty. You may still get credit, but you may face stricter terms or higher interest costs.

Some insurance companies also use credit information. They may use it to help decide whether to offer a policy and what premium to charge. These insurance‑specific scores are sometimes called credit based insurance scores.

Quick Navigation

- How Credit Scores Work

- Key Factors That Shape a Credit Score

- Why Credit Scores Matter

- Credit Score Examples

- Credit Scores and Major Life Decisions

- Common Credit Score Myths

- Where To Learn More

- FAQ: Credit Scores

- Recent Guides and Articles on Financial Concepts

- Online Calculators and Free Tools You Can Download

How Credit Scores Work

Credit scores work by turning the information in your credit reports into a single number that reflects your creditworthiness. [2] Scoring models read your credit history and estimate how likely you are to repay borrowed money. Most scores range from 300 to 850, so higher numbers signal lower risk.

Because lenders want a consistent way to judge risk, many of them use FICO Scores. These scores rely on data from the three major credit bureaus. Each bureau keeps its own records, so your score can differ across them. Differences in timing, reporting practices, and scoring model versions also create natural variation.

Lenders then use credit scores to help decide whether to approve applications and what terms to offer. A higher score can lead to lower interest rates and higher credit limits. A lower score can lead to stricter conditions. Since each lender sets its own risk standards, there is no universal cutoff.

Your score also changes as your credit report changes. New payments, updated balances, new accounts, and credit inquiries all influence the information that scoring models use. As a result, the score you saw last month may not match the score a lender sees today.

Other credit scores exist as well. Some are designed for consumers, while others are built for specific industries. They may weigh information differently from FICO Scores. This is why the score you buy online may not match the score a lender uses.

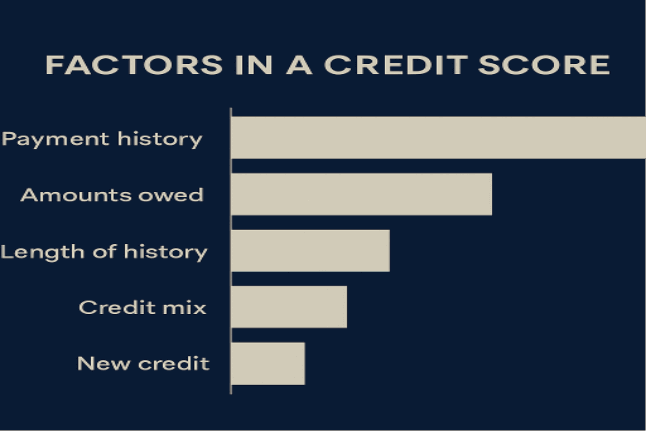

Key Factors That Shape a Credit Score

Credit scores reflect several parts of your credit history. Scoring models group this information into broad categories and weigh each one differently. [3] Together, these categories help estimate how likely you are to repay borrowed money.

Payment history carries the most weight. It shows whether you have paid past credit accounts on time. Because lenders want to understand repayment behaviour, scoring models place strong emphasis on this pattern.

Amounts owed also play a major role. This category looks at how much of your available credit you are currently using. Scoring models read this number to understand how heavily you rely on credit at any moment.

Length of credit history adds another layer. Longer histories give scoring models more information about your borrowing behaviour. They consider the age of your oldest account, the age of your newest account, and the average age of all accounts.

Credit mix helps scoring models see the types of credit you have used. This may include credit cards, instalment loans, retail accounts, or mortgage loans. A broader mix gives models a clearer picture, but it is not required for a strong score.

New credit completes the picture. When you open new accounts or when lenders check your credit, scoring models record these events. They use this information to understand how often you seek new credit and how recently you have done so.

These categories work together to form your credit score. They do not guarantee any outcome, but they give lenders a structured way to assess financial risk.

Why Credit Scores Matter

Credit scores matter because they help businesses understand financial risk. Lenders use this number to estimate how likely you are to repay borrowed money. When you apply for a loan or a credit card, it becomes one of the first signals they review.

Scores also shape the terms you receive. A stronger record can make it easier to qualify for credit and may lead to lower interest rates. A weaker record can result in stricter conditions and higher borrowing costs. Because each lender sets its own standards, the impact of your score can vary from one application to the next.

The influence extends beyond borrowing. Many landlords check credit information when reviewing rental applications. Utility providers may do the same before opening new accounts. In some regions, insurance companies also use this information to help set premiums. These checks give businesses a clearer view of how reliably you have managed financial commitments in the past.

Taken together, these uses show why this number plays a role in many financial decisions. It gives businesses a structured way to assess risk and helps them decide how to work with new customers.

Credit Score Examples

Examples help show how scoring models interpret different patterns in a credit report. These simple scenarios highlight how models read behaviour and compare it with the profiles of similar borrowers. [4]

Example 1: A strong repayment record

A person who pays bills on time and avoids missed payments shows a steady pattern. Scoring models read this history as lower risk because it signals reliable repayment. As a result, the number tends to sit in a stronger range.

Example 2: High balances relative to limits

Another person may pay on time but use most of their available credit. Scoring models see this as heavy reliance on borrowing. Because the amount owed sits close to the credit limit, the number may fall into a more moderate range.

Example 3: Short or limited history

Someone new to credit may have only one or two accounts. Scoring models have less information to work with, so the number may shift more as new data appears. A short history can place the score in a developing range until more information builds.

Example 4: Several recent applications

A person who applies for multiple new accounts in a short period creates a cluster of inquiries. Scoring models record these events and may treat them as a sign of increased risk. As a result, the number may move into a more cautious range for a time.

Example 5: Many accounts of the same type

Another person may hold several credit card accounts but few other types of credit. Scoring models consider this mix and may view a narrow set of accounts differently from a more varied profile. This can influence where the number sits within the broader range.

Together, these examples show how scoring models interpret different behaviours. They do not predict any specific outcome, but they help illustrate how information in a credit report shapes the number lenders use to assess financial risk.

Credit Scores and Major Life Decisions

Credit information influences many major financial decisions. When you apply for a home loan, lenders review your history to understand how you have managed credit over time. They use this number to judge risk and to set the terms of the loan. As a result, a stronger record can make the process more straightforward, while a weaker one may lead to tighter conditions.

This review continues when you buy a car. Auto lenders look at the same information to estimate how likely you are to repay the loan. Their assessment shapes both approval decisions and the interest rate you receive. Because car loans often involve large amounts, even small changes in the rate can affect the total cost.

Credit information also matters when you rent a home. Many landlords check it to see how reliably you have met financial commitments in the past. This helps them decide whether to approve an application or request additional documentation.

In some regions, insurance companies use credit data as well. They may consider it when setting premiums for certain types of policies. These checks help them understand risk in the same way lenders do.

Credit information can also influence business decisions. When you apply for a small business loan or a line of credit, lenders often review your personal credit history. They use it to understand how you have handled financial obligations and to set the terms of the funding.

Taken together, these situations show how credit information connects to many life events. It gives businesses a structured way to assess risk and helps them decide how to work with new customers.

Common Credit Score Myths

Misunderstandings about credit information appear often, and they can make the scoring process seem more complex than it is. Clearing up these myths helps show how scoring models actually work and what they do and what they do and do not consider. [5]

Myth 1: A score alone decides whether you get credit

This idea oversimplifies how lenders make decisions. In practice, lenders review several details, including income, employment history, and overall debt levels. They treat the score as one input among many, not the final verdict.

Myth 2: A poor score follows you forever

This belief exaggerates the impact of past issues. A score reflects your risk at a specific moment, and it changes as new information enters your credit report. Older problems matter less over time, and the number shifts as your history evolves.

Myth 3: Scoring systems treat people unfairly

Some assume that personal characteristics influence the number. Scoring models do not use factors such as race, gender, or nationality. Laws like the Equal Credit Opportunity Act prohibit lenders from considering this information. Models focus only on credit‑related data.

Myth 4: Scoring invades your privacy

Another misconception is that scoring adds new layers of data collection. In reality, models use the same information lenders already review—your credit report, your application, and your bank file. The score simply summarises this information into a single number.

Myth 5: Applying for new credit always lowers your score

Applications can create inquiries, but the effect is often smaller than people expect. Scoring models treat multiple auto or mortgage inquiries within a short period as a single event. They also ignore inquiries tied to account monitoring or prescreened offers.

Taken together, these myths show how easy it is to misunderstand the scoring process. Understanding what models consider—and what they ignore—helps explain why the number can vary across situations.

Where To Learn More

Understanding how credit information works becomes easier when you can explore related topics in one place. This guide introduces the core ideas, and the References and Further Reading section below lists the sources used throughout the page so you can dive deeper into the material at your own pace.

For quick definitions of key terms, the MoneyOpes Financial Dictionary offers clear explanations written for a global audience. It covers concepts that appear throughout this guide.

If you want to see how credit information shapes real financial decisions, the MoneyOpes guide on improving your score for a home loan shows how a stronger record can make borrowing cheaper and easier. With better rates, more lender interest, and greater negotiating power, a high score can open the door to deals that most borrowers never see.

Together, these resources give you a broader view of how credit information fits into everyday financial decisions and where it shows up across the borrowing process.

FAQ: Credit Scores

What is a credit score?

A credit score is a number that summarises the information in your credit report. Lenders use it to estimate risk and to help decide how to work with new customers.

What factors shape a credit score?

Scoring models look at several details, including payment history, amounts owed, length of history, credit mix, and new credit. Each factor contributes differently to the final number.

How does a credit score influence major financial decisions?

Credit information appears in many life events. Lenders review it when you apply for a home loan or car loan, landlords may check it when you rent, and some insurers consider it when setting premiums.

Do all credit scores look the same?

No. Different scoring models weigh information differently, so the number you see online may not match the one a lender uses. This variation is normal because each model interprets the same report data in its own way.

References and Further Reading

[1] Federal Trade Commission. “Credit Scores”

[2] Fair Isaac Corporation. “Credit Scores”

[3] Fair Isaac Corporation. “What’s in my FICO® Scores?”

[4] Federal Trade Commission. “Credit Score”

[5] Fair Isaac Corporation. “Credit score facts & fallacies”

Recent Guides and Articles on Financial Concepts

-

Emergency Fund Calculator and Guide

An emergency fund gives you a simple way to prepare for unexpected costs. The emergency fund calculator included on this page shows you how much you may…

-

Insurance Basics: How Insurance Protects You

Insurance helps protect you from the financial impact of unexpected events. It works through a simple idea. You enter into a contract with an insurance company, and…

-

APR and APY: What They Mean and Why They Matter

Understanding the difference between APR vs APY helps you compare borrowing and saving choices with confidence. These two terms look similar at first. Even so, they measure…

-

What is Interest

Interest affects many everyday money choices. Many people still want a clear explanation of what is interest and why it matters. The definition of interest is simple.…

-

What is Inflation

Inflation measures how much more expensive a set of goods and services has become over a certain period. The International Monetary Fund explains inflation as the change…

Online Calculators and Free Tools You Can Download

Each calculator gives you one way to test money scenarios. You can also compare other tools. Use the buttons below to explore more calculators or downloadable options. This lets you look at loan, saving, and investment choices side by side.