|

⏱️ Estimated time to read:

Insurance helps protect you from the financial impact of unexpected events. It works through a simple idea. You enter into a contract with an insurance company, and the company agrees to cover certain costs if something goes wrong. [1] This contract is called a policy. It explains what is covered, when payments apply, and how much support you may receive.

Insurance matters because it reduces the stress of emergencies, accidents, illness, or damage to your property. It creates a safety net that supports you and your long term plans. As you learn these insurance basics, you will see how insurance works across different situations. You will also see how each type of coverage offers its own form of protection.

This guide introduces the core ideas behind insurance. It explains key terms, shows how policies operate, and outlines the main types of coverage you may come across. It aims to give you clear information so you can understand your options at your own pace.

Table of Contents

- A Brief History of Insurance

- How Insurance Works

- Types of Things That Can Be Insured

- Glossary: Insurance Basics

- Conclusion

- FAQ Insurance Explained

- Recent Guides and Articles on Financial Concepts

- Latest Free Tools You Can Download

A Brief History of Insurance

People have used different forms of insurance for thousands of years. Early records from ancient Babylon show merchants using agreements that protected them from losses during long trading journeys. [2] These early contracts helped people share risk. They also gave traders more confidence to move goods across long distances. When you look at these early examples, you can see the first signs of how insurance works in practice.

Insurance changed as societies faced new risks. After the Great Fire of London in 1666, people created organized fire insurance groups. [3] They wanted protection from large losses that could destroy homes and businesses. Later, new tools for understanding life expectancy supported the first life insurance plans. These developments shaped many of the insurance basics used today.

Insurance reached the United States by the late 1600s. By 1752, Benjamin Franklin helped form the Philadelphia Contributionship. [2] It offered fire protection at a time when many homes were built from wood. Other groups soon followed. Some supported specific communities. Others focused on new types of coverage. As time passed, insurance expanded across many countries and adapted to new needs.

Today, insurance is a global industry. People can compare plans online and choose options that fit their situation. Even with these changes, the core idea remains the same. Insurance reduces the financial impact of unexpected events. [1] Simply put, insurance protects you in everyday life.

How Insurance Works

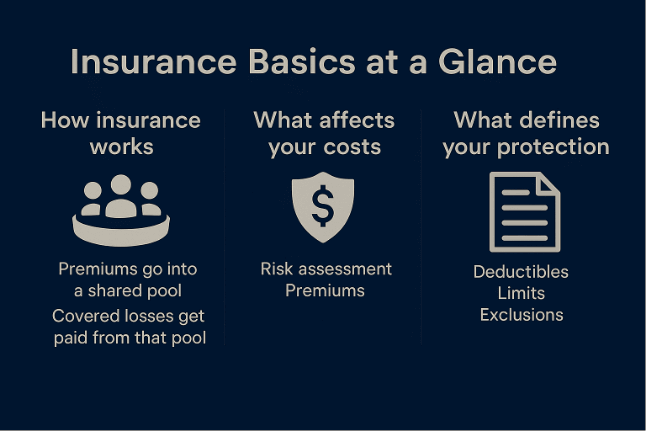

Insurance basics works through a simple idea. People pool their money to protect each other from unexpected losses. First, you pay a premium into this pool. Then, when someone experiences a covered event, the insurance company uses that pool to help pay the cost. [4] This shared approach reduces the financial pressure of accidents, illness, or property damage. In addition, it shows how insurance works by turning a large and potentially life changing loss into an affordable one. This being achieved through payment of a premium, and spreading of risk, which remains the core part of insurance basics.

The Structure of a Policy

A policy sets out the rules of your coverage. First, it explains what the insurer will pay for and what it will not. Next, the declarations page lists key details such as coverage limits and active dates. Then, the insuring agreement describes the protection you receive. Exclusions set boundaries, while endorsements let you add extra protection when you need it. As you read these parts together, you get a clear view of your benefits and see your insurance coverage explained in detail.

Risk Assessment and Claims

Insurance companies assess risk before they offer a policy. They review factors such as age, location, driving history, property condition, or health information. From this, these details help them decide the price of your premium. Actuaries then use data to estimate how likely a claim is and set prices that keep the company stable.

When a covered event occurs, you file a claim. The insurer reviews the information and decides how much to pay based on the policy. Some claims require an adjuster to inspect the damage. Others move directly between the insurer and the service provider. If you disagree with the outcome, most policies offer ways to appeal. Through this process, you can see how insurance protects you and why clear policy terms matter.

Insurance also operates under state and federal rules. Consequently, these regulations help protect consumers and ensure companies can pay claims. They guide how policies are written, how premiums are set, and how disputes are resolved. As a result, with these safeguards in place, insurance continues to offer a reliable way to manage risk and support long term financial stability.

Types of Things That Can Be Insured

Insurance can protect many parts of life. Most coverage falls into two broad groups: property and casualty insurance and life and annuity insurance. [2] These groups include familiar areas such as automobile, fire, health, homeowners, life and annuity, marine, and travel insurance. They form the base of the industry and support many everyday needs.

Today, insurance reaches far beyond these traditional categories. People insure digital assets, financial assets, and valuable equipment. Some plans even cover pets, events, or specific body parts. Therefore, as lifestyles and technology evolve, insurers continue to create new products. This variety shows how flexible insurance has become and how it adapts to modern risks, yet the fundamental insurance basics of paying a premium and pooling risk continue to work the same way.

Glossary: Insurance Basics

Core Policy Features

- Coverage

- Coverage describes what the insurer agrees to pay for. It may include damage to property, medical costs, or liability claims. Specifically, each policy lists its own coverage details and conditions.

- Deductible

- A deductible is the amount you pay out of pocket before the insurer contributes. A higher deductible often leads to a lower premium. On the other hand, a lower deductible usually means you pay more for the policy.

- Endorsement

- An endorsement is an addition to your policy that changes or expands your coverage. It can add protection for risks not included in the standard policy. For example, you may add flood coverage to a homeowners policy.

- Exclusion

- An exclusion is something the policy does not cover. Common exclusions include wear and tear, intentional damage, or certain natural events. Exclusions help define the boundaries of your protection.

- Policy Limit

- The policy limit is the maximum amount the insurer will pay for a covered loss. Limits vary by policy type and coverage level. Higher limits offer more protection but often cost more.

- Premium

- A premium is the amount you pay to keep your insurance policy active. You may pay it monthly, quarterly, or yearly. Therefore, as you pay premiums, you support the pool of money that covers losses for everyone in the plan.

People and Processes in Insurance

- Beneficiary

- A beneficiary is the person who receives the payout from a life insurance policy. Policyholders choose their beneficiaries when they set up the plan.

- Claim

- A claim is a request for payment after a covered event. First, you file a claim when you experience a loss. Then, the insurer reviews the details and decides how much to pay based on the policy.

- Insurer

- The insurer is the company that provides the policy. It collects premiums and pays claims according to the contract. In addition, insurers manage risk across many policyholders.

- Policyholder

- The policyholder is the person or business named on the policy. This person has the right to make changes, file claims, and receive benefits.

- Term

- The term is the length of time the policy remains active. Some policies renew each year. Others, such as term life insurance, last for a set number of years.

- Underwriting

- Underwriting is the process insurers use to assess risk before offering a policy. They review factors such as age, location, property condition, or driving history. As a result, these assessments help determine your premium.

Conclusion

Insurance works through a simple idea. People pool their money so no one faces a major loss alone. Throughout the article, you saw how this idea takes shape in real policies. Premiums, deductibles, limits, exclusions, and endorsements all work together to decide how much protection you receive and how much you pay. As the article explained how insurance works, it also showed how insurers assess risk, set prices, and review claims. As a result, you get a clearer view of your benefits and see your insurance coverage explained in straightforward terms.

The article also showed how many things people insure today, from everyday needs to newer digital and financial assets. Even with this wide range, the fundamental mechanics of insurance basics remain the same. The glossary then tied these ideas together by giving simple definitions of the terms that appear across most policies. Taken together, the article showed that while insurance continues to adapt to modern risks, its purpose remains the same. To share financial risk so individuals do not face large losses on their own.

FAQ Insurance Explained

Insurance basics include how premiums, deductibles, limits, exclusions, and endorsements work together to shape your protection. These features decide how much you pay and what your policy covers.

Insurance works by pooling money from many people so no one faces a major loss alone. Therefore, when you pay a premium, you join that pool. As a result, if you experience a covered loss, the insurer uses the pool to help pay for it.

Insurers assess risk, review your information, and consider the likelihood of a claim. As they evaluate these factors, they set a premium that reflects the level of risk and the type of coverage you choose.

Deductibles decide how much you pay before your insurer contributes, while limits cap how much the insurer will pay. Together, they shape your benefits and help you see your insurance coverage explained in clear terms.

Exclusions outline what your policy does not cover, and endorsements adjust your coverage by adding or changing specific protections.

References and Further Reading

[1] Metropolitan Life Insurance Company. “What is Insurance”

[2] Library of Congress. “Insurance History”

[3] London Museum. “How the Great Fire of London Created Insurance”

[4] Legal Clarity. “How Does Insurance Work and What Are Its Key Components?”

Recent Guides and Articles on Financial Concepts

-

Emergency Fund Calculator and Guide

An emergency fund gives you a simple way to prepare for unexpected costs. The emergency fund calculator included on this page shows you how much you may…

-

What Is a Credit Score

A credit score is a number that shows how likely you are to repay borrowed money. Lenders use this number because it gives them a quick way…

-

APR and APY: What They Mean and Why They Matter

Understanding the difference between APR vs APY helps you compare borrowing and saving choices with confidence. These two terms look similar at first. Even so, they measure…

-

What is Interest

Interest affects many everyday money choices. Many people still want a clear explanation of what is interest and why it matters. The definition of interest is simple.…

-

What is Inflation

Inflation measures how much more expensive a set of goods and services has become over a certain period. The International Monetary Fund explains inflation as the change…

Latest Free Tools You Can Download

-

Business Loan Affordability Calculator for Commercial and Industrial Property

This business loan affordability calculator is an Excel template that helps users test DSCR, compare repayments,…

-

Ratio Analysis Spreadsheet

A simple Excel spreadsheet that helps you calculate and understand key business financial ratios. Ideal for…

Disclaimer – Educational Use Only

Content on MoneyOpes.com is for informational and educational purposes only. It does not constitute financial, legal, or professional advice. Your financial situation is unique, and outcomes may differ. Past performance is not a guarantee of future results. MoneyOpes.com adheres to strict editorial integrity standards, and to the best of our knowledge, all content is accurate as of the date posted. See our full disclaimer.