|

⏱️ Estimated time to read:

Asset allocation is the way you divide your money across broad groups of investments such as stocks, bonds, cash, and alternative assets. Alternatives can include real estate, commodities, and art, although many traditional models either exclude them or treat them as optional. Overall, this mix forms your asset allocation strategy, and it shapes both how your portfolio grows and how much it moves during market swings.

When explaining asset allocation for beginners, the key is understanding how each asset class behaves. Stocks can rise and fall quickly. Bonds tend to move more steadily. Cash stays stable but grows slowly. Alternatives vary widely in risk and liquidity. Therefore, by combining these groups, you create a balance between growth and stability that reflects your goals.

Your allocation should match your time horizon, your financial goals, and your comfort with risk. A long timeframe often supports a higher share of growth assets. However, a shorter timeline usually calls for more stability. Therefore, as your situation changes, your mix may need to shift as well. This guide explains what asset allocation means, outlines the main asset classes, and shows why your mix matters. In addition, it walks through how to choose an allocation, introduces common strategies, and gives simple examples for different ages and portfolio sizes. Finally, it ends with how rebalancing helps keep your mix aligned over time.

Table of Contents

- What Is Asset Allocation

- Main Asset Classes

- Why Is Asset Allocation Important

- How to Choose an Asset Allocation

- Common Asset Allocation Strategies

- Examples of Asset Allocation

- Rebalancing

- Conclusion – Bringing It All Together

- FAQ Asset Allocation For Beginners

- Recent Articles on Market Concepts

- Explore More Investing Resources And Tools

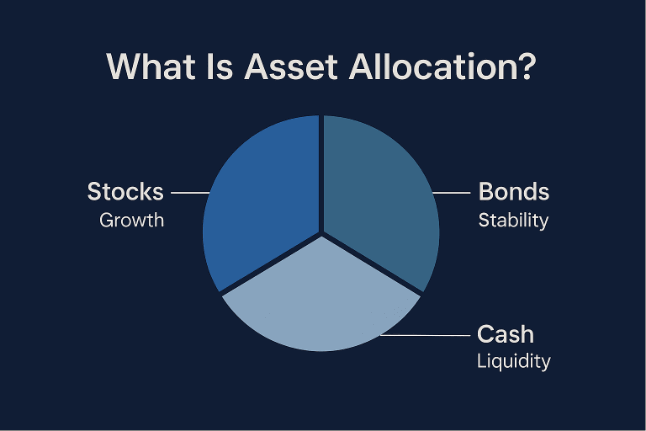

What Is Asset Allocation

Asset allocation means dividing your investments across broad asset groups such as stocks, bonds, and cash. [1] This mix forms your asset allocation strategy, and it helps you balance growth and stability as markets move. Each asset class behaves differently. Stocks can grow faster but also move more sharply. Bonds tend to move more steadily. Cash stays stable but grows slowly.

In beginner asset allocation, the focus is on building a simple structure that matches your goals and your comfort with risk. Your time horizon also matters because it shapes how much movement you can accept along the way. These factors change over time, so your mix may shift as your life changes.

A clear allocation helps you stay focused on long term plans rather than short term market swings. It also gives you a straightforward way to manage your portfolio as markets rise and fall.

Main Asset Classes

Asset allocation works by spreading your money across several broad groups of investments. These groups behave differently as markets rise and fall. Therefore, combining them helps you build a simple asset allocation that balances growth and stability. The SEC explains that most portfolios start with stocks, bonds, and cash. [1] However, many investors also explore alternatives, although these assets come with their own risks and may not appear in every asset allocation strategy.

Stocks

Stocks give you ownership in a company. They offer the strongest potential for long term growth because companies can expand and increase profits. In addition, they move the most from year to year. Therefore, stocks can rise quickly, yet they can also fall sharply. For example, large company stocks, have lost money in many individual years, and some losses have been significant. Even so, investors who stay invested over long periods often see strong positive returns. As a result, stocks act as the main growth driver in a portfolio.

Bonds

Bonds are loans to governments, cities, or companies. They usually move more steadily than stocks and offer more modest returns. Therefore, because they tend to fluctuate less, many investors increase their bond holdings as they approach a financial goal. Some bonds, such as high yield bonds, offer higher returns but also carry higher risk. Bonds help steady your portfolio and reduce overall swings.

Cash and Cash Equivalents

Cash and cash equivalents include savings accounts, certificates of deposit, Treasury bills, money market accounts, and money market funds. These investments focus on safety. However, they offer the lowest returns of the major asset classes, but the chance of losing money is very low. Moreover, some cash equivalents are backed by governments, which adds another layer of protection. The main risk is inflation, which can erode returns over time. Even so, cash helps you preserve value and manage short term needs.

Alternatives

Alternatives include real estate, precious metals, commodities, private equity, and other nontraditional assets. These assets behave differently from stocks, bonds, and cash. They can add variety to a portfolio. However, they also come with category specific risks. For instance, some alternatives are less liquid. While, others can move sharply in response to economic events. Because of these differences, many traditional models treat alternatives as optional rather than core holdings.

Why Is Asset Allocation Important

Asset allocation matters because it drives most of your long term investment results. Therefore, your mix of stocks, bonds, cash, and other assets shapes how much your portfolio can grow and how much it may move when markets shift. In addition, a clear asset allocation strategy helps you manage risk while still giving your money room to grow.

Your goals play a central role in choosing the right mix. When you build a simple asset allocation, you first look at what you are saving for and how much time you have. A goal that sits only five years away, such as saving for college, usually calls for a more conservative mix because you have less time to recover from market drops. On the other hand, a goal that sits thirty years away, such as retirement, often supports a higher share of growth assets because you can ride out more market movement.

Asset allocation stays important as your life changes. Your goals shift, your time horizon shortens, and your comfort with risk may rise or fall. Adjusting your mix keeps your plan aligned with where you are and where you want to go.

How to Choose an Asset Allocation

Choosing an asset allocation starts with understanding your situation. A clear mix helps you balance growth and stability, and it keeps your plan aligned with your goals. You build this mix by looking at three core factors. Specifically, your time horizon, your goals, and your comfort with risk. These factors shape every asset allocation strategy, including simple asset allocation and portfolio allocation for beginners.

Time Horizon

Your time horizon shows how long your money can stay invested. A longer horizon lets you hold more growth assets because you have time to recover from market swings. A shorter horizon pushes you toward steadier assets such as bonds and cash. This shift helps protect your savings as the date you need the money gets closer.

Goals

Your goals guide how you shape your mix. When you save for a short term goal, such as buying a car in two years, you usually choose a more conservative allocation. Simply put, you want stability because you cannot afford large swings. Howver wen you save for a long term goal, such as retirement in thirty years, you can include more growth assets because you have time to ride out market movement. As your goals evolve, your allocation should evolve as well.

Risk Comfort

Your comfort with risk affects how much movement you can accept in your portfolio. Some investors feel comfortable with larger swings if it means more growth potential. While, others prefer steadier returns even if growth is slower. Therefore, matching your allocation to your comfort level helps you stay invested through different market conditions.

Your comfort with risk shapes how much movement you can accept in your portfolio. If you want a quick sense of your investing style, you can take the Investor Personality Test. It takes about two minutes and is for learning only.

Common Asset Allocation Strategies

Common strategies help you build a mix that fits your goals, your time horizon, and your comfort with risk. These approaches also support simple asset allocation and portfolio allocation for beginners, because they give you clear ways to balance growth and stability as your life changes.

- Age‑based allocation — Investors often adjust their mix as they move through different stages of life. Therefore, when you are younger, you usually hold more growth assets because you have time to recover from market swings. However, as you get closer to using the money, you shift toward steadier assets. This shift creates a clear path from higher growth to higher stability.

- Goal‑based allocation — Your goals guide how you shape your mix. When you save for a short term goal, you usually choose a more conservative allocation because you cannot afford large swings. When you save for a long term goal, you can include more growth assets because you have time to ride out market movement. As your goals change, your mix changes with them.

- Risk‑based allocation — Your comfort with risk influences how much movement you can accept in your portfolio. Some investors accept larger swings for more growth potential. Others prefer steadier returns even if growth is slower. When you match your mix to your comfort level, you stay invested more easily through different market conditions.

These strategies often work together. You may start with an age‑based approach, adjust it for your goals, and then refine it based on your comfort with risk. This combination creates a practical asset allocation strategy that adapts as your life evolves.

Examples of Asset Allocation

Examples help show how different mixes work in practice. These simple allocations illustrate how time horizon, goals, and risk comfort shape a basic asset allocation strategy. In addition, they also give beginners to asset allocation a clear starting point before adjusting for their own situation.

Short Time Horizon (about 2–5 years)

A short horizon usually calls for more stability because you have less time to recover from market swings. Therefore, a mix might look like:

- 20% stocks — Some growth potential

- 50% bonds — Steadier movement

- 30% cash and cash equivalents — High stability for near term needs

This type of mix suits goals such as buying a car or building a home deposit.

Medium Time Horizon (about 10–15 years)

A medium horizon allows for more growth while still managing risk. A mix might include:

- 50% stocks — Balanced growth

- 35% bonds — Smoother returns

- 15% cash — Short term stability

This structure works for goals such as funding education or building long term savings.

Long Time Horizon (20–30 years or more)

A long horizon supports a higher share of growth assets because you have time to ride out market movement. As a result, a mix might look like:

- 70% stocks — Strong long term growth potential

- 25% bonds — Added stability

- 5% cash — Short term needs

This approach suits long term goals such as retirement.

Adding Alternatives

Some investors include alternatives such as real estate, commodities, or other assets. These can add variety, yet they also bring category specific risks. A simple example might be:

- 60% stocks

- 25% bonds

- 10% alternatives

- 5% cash

Alternatives can change how a portfolio behaves. For this reason, they often appear in more advanced mixes rather than beginner allocations.

Rebalancing

Rebalancing restores your portfolio to the mix you originally planned. [2] As markets move, some investments grow faster than others, and your simple asset allocation can drift. By rebalancing, you bring your portfolio back to a level of risk that matches your goals and keep one asset class from taking over.

First, start by checking whether any part of your portfolio has grown far beyond its target. Then, when that happens, you can sell part of the overweighted asset and shift the proceeds into areas that have fallen behind. In addition, you can also direct new contributions toward the underweighted parts of your portfolio until the mix returns to balance. As a result, these steps keep your allocation aligned with your plan as markets rise and fall.

Timing plays a key role. Some investors rebalance on a set schedule, such as every six or twelve months. While, others wait until an asset class moves beyond a preset range. Either approach prevents your mix from drifting too far. Rebalancing can feel counterintuitive because it often means trimming recent “winners” and adding to recent “losers,” yet this discipline helps you buy low and sell high.

However, before you make changes, you consider any transaction costs or tax effects that may apply. Understanding these costs helps you choose the most efficient way to bring your portfolio back to target.

You can also rebalance by directing new contributions toward the underweighted asset class instead of selling anything. This approach works well when you want to avoid transaction costs or tax effects.

Conclusion – Bringing It All Together

A clear asset allocation pulls every part of your investing plan into one cohesive structure. You choose a mix of stocks, bonds, cash, and alternatives based on your time horizon, your goals, and your comfort with risk. As a result, this mix becomes the backbone of your simple asset allocation. As markets move and your life evolves, this structure helps you stay focused on long term growth while managing the level of risk you take on.

Each decision builds on the last. First, start by defining what you are saving for and how long you have. Then, match your allocation to your comfort with market ups and downs, creating a mix that feels realistic and sustainable. Therefore, as your goals shift, whether you move closer to retirement, plan for a major purchase, or adjust your priorities, you update your allocation so it continues to reflect your needs.

Rebalancing keeps everything aligned. Markets naturally push your portfolio away from its targets. Therefore rebalancing brings it back to the risk level you intended. As a result, this discipline reinforces your strategy. So, prevents your mix from drifting too far, and supports steadier progress toward your goals.

Together, these steps form a flexible long term framework that guides your investing plan, keeps your mix aligned with your goals, and helps you stay steady through market changes.

A clear asset mix, steady adjustments, and timely rebalancing keep your investing plan focused and on track.

Quick Summary

- Choose an asset mix that reflects your time horizon, your goals, and your risk comfort.

- Adjust the mix as your goals shift and your timeline changes.

- Rebalance to keep your portfolio aligned with your simple asset allocation and your intended level of risk.

FAQ Asset Allocation For Beginners

A simple asset allocation gives your portfolio a clear structure that reflects your goals, your time horizon, and your comfort with risk. As a result, it guides how you spread your money across stocks, bonds, and cash, and it helps you stay focused as markets rise and fall.

Your asset mix drifts because different investments grow at different speeds. Therefore, as one part of your portfolio outperforms the others, your original simple asset allocation shifts and your risk level increases. This drift happens gradually, even when you make no trades.

Rebalancing restores your target mix by trimming the parts that have grown too large and adding to the parts that have fallen behind. By bringing your allocation back to its intended shape, you keep to your asset allocation strategy. Therefore, keeping with your long term plan and your preferred level of risk.

You adjust your allocation when your goals change, your timeline shortens, or your comfort with risk evolves. Therefore, as your life moves forward, updating your mix ensures your asset allocation continues to match what you are working toward.

There is no single best asset allocation for beginners because every investor starts with different goals, timelines, and levels of comfort with risk. As a result, a simple asset allocation works best when it reflects your own circumstances. For instance, your age influences how much growth you can pursue, your goals shape how much stability you need, and your risk comfort determines how much market movement you can handle. When you combine these factors, you end up with a mix that fits you rather than a one size fits all formula.

References and Further Reading

[1] US Securities and Exchange Commission. “Difference Between a Loan Interest Rate and the APR”

[2] US Securities and Exchange Commission. “Asset Allocation, Diversification, and Rebalancing 101”

Recent Articles on Market Concepts

-

Market Cycle Phases: How Markets Rise, Peak, Fall, and Recover

Markets move in patterns that repeat over time. These patterns…

-

How Diversification Reduces Risk in Investing

Diversification helps investors manage uncertainty by spreading exposure across different…

-

Risk vs Return: Understanding the Trade Off in Investing

Understanding risk vs return is one of the first steps…

Explore More Investing Resources And Tools

Use calculators and downloadable tools, such as our ratio analysis spreadsheet to apply what you learn.

Market Concepts – Tools to Download and Online Calculators

Market Concepts – Recent and Most Read Articles and Guides

Disclaimer – Educational Use Only

Content on MoneyOpes.com is for informational and educational purposes only. It does not constitute financial, legal, or professional advice. Your financial situation is unique, and outcomes may differ. Past performance is not a guarantee of future results. MoneyOpes.com adheres to strict editorial integrity standards, and to the best of our knowledge, all content is accurate as of the date posted. See our full disclaimer.